Posted on 13 Mar 2026

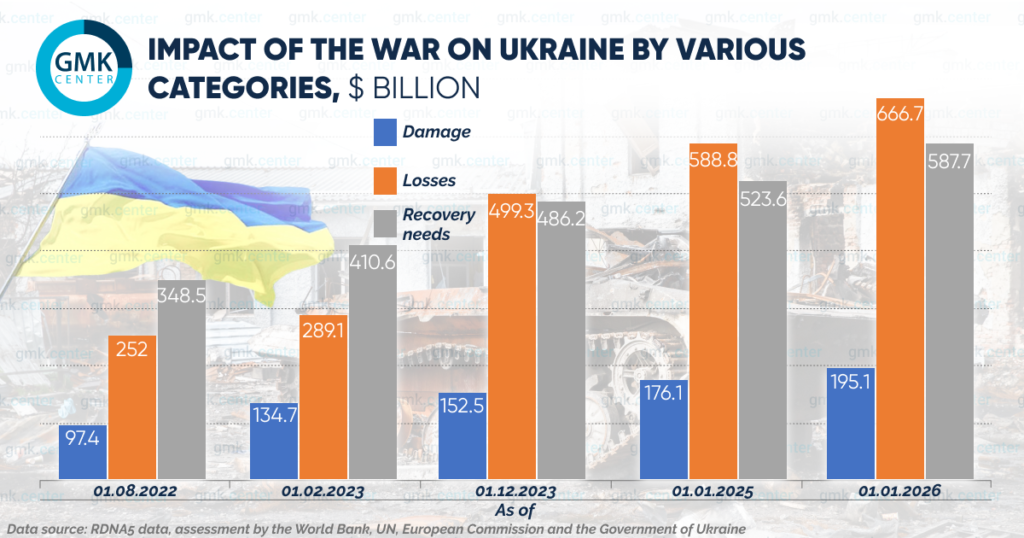

Direct losses from the war exceeded $195 billion, while reconstruction needs amounted to $588 billion. The iron and steel indudtry was one of the most affected industries: most indicators fell by 50–70%.

GMK Center analyzed the losses suffered by the industry and the role of the iron and steel industry in post-war reconstruction.

According to World Bank estimates (RDNA5 report), Ukraine’s direct losses over four years of war exceeded $195 billion (in a previous estimate as of February 2025, they amounted to $176 billion). Total losses from the war reached $667 billion.

Ukraine’s reconstruction needs over a ten-year horizon amount to $588 billion, almost three times the country’s nominal GDP in 2025. The largest investments will be needed for transport (over $96 billion), energy ($91 billion), and housing ($90 billion).

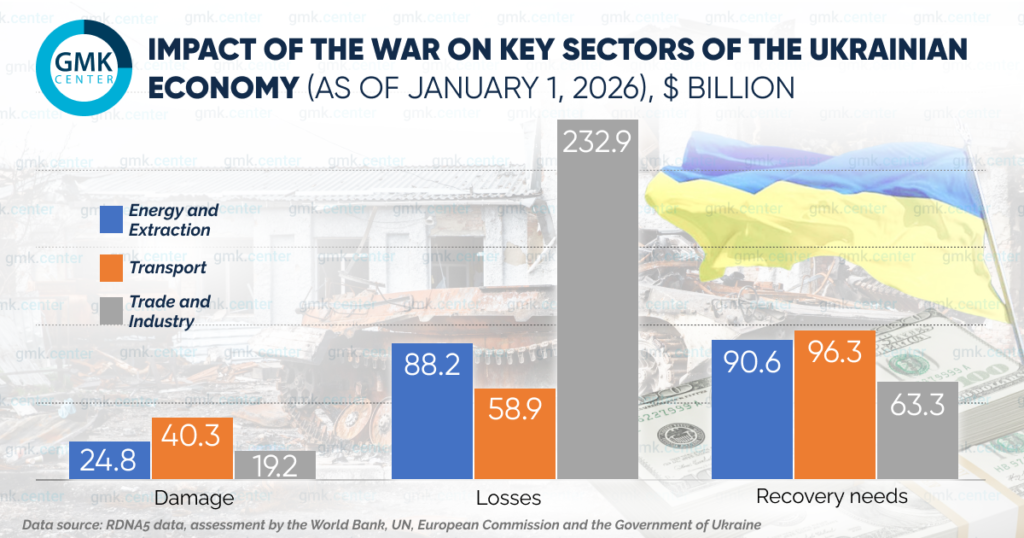

Direct losses in energy and energy production are estimated at $24.8 billion, of which the largest share ($17.1 billion) is in energy. Losses in this sector due to reduced demand and limited infrastructure operation amounted to $88.2 billion. The total cost of restoration is estimated at $90.6 billion, mainly for the reconstruction of the energy system ($70.8 billion).

Total losses to industry and trade amount to $19.2 billion, of which 85% are losses to the industrial sector. Damage has been recorded in five industrial and frontline regions: Donetsk, Kharkiv, Kyiv, Zaporizhzhia, and Mykolaiv (over 80% of total losses). The losses are estimated at $232.9 billion, which exceeds the pre-war GDP. They are caused by a decline in demand and exports, power outages, and logistical disruptions. The total reconstruction needs for 2026–2035 amount to $63.3 billion.

Total losses in the transport sector amount to $40.3 billion. The largest losses were recorded on railways (32%), local roads (23%), and highways (20%). In 2025, 90% of new damage was to railway infrastructure. Losses of $58.9 billion are mainly related to the blockade of Black Sea ports (60%). The cost of restoration for 2026–2035 is $96.3 billion (a 24.2% increase over RDNA4).

Explanation of terms

Direct losses – costs of restoring destroyed or damaged physical assets and infrastructure, estimated in monetary terms at pre-conflict prices.

Losses – changes in economic flows due to war (service interruptions, lost income, additional costs), expressed in monetary terms.

Recovery needs – the cost of repair, restoration, and reconstruction, taking into account the principle of “Build Back Better,” inflation, and other factors, expressed in market prices at the end of the reporting period.

According to KSE estimates, Ukraine’s total economic losses from the war in terms of lost revenue at the beginning of 2026 amounted to $1.7 trillion, with losses in added value amounting to $0.6 trillion. The most affected sectors of the economy were trade ($696.3 billion), industry, construction, and services ($645.6 billion), as well as agriculture ($81.9 billion). Losses in energy infrastructure amounted to $75.3 billion, and in logistics – $60.2 billion.

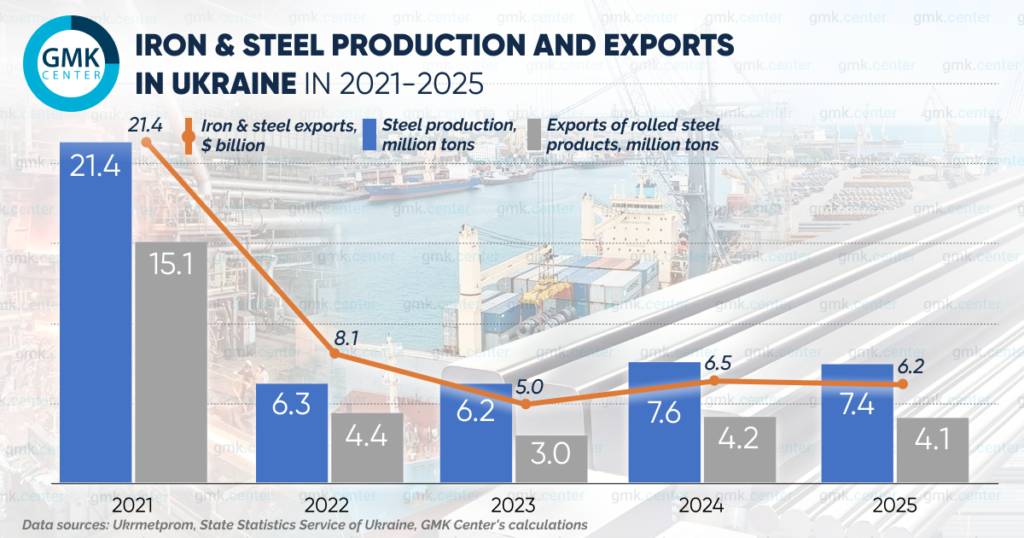

One of the sectors of the economy that has suffered most from the war is the iron and steel industry. The war has dealt a severe blow: the destruction of the Azovstal and Ilyich steelworks in Mariupol has led to the loss of 40% of steel production capacity. Total steel production over four years has fallen by 65% compared to pre-war levels, with output dropping to 7 million tons per year from 21 million tons in 2021. Companies in the industry have been forced to quickly reorient themselves to other markets and sources of raw materials and to restructure their logistics.

As a result of the full-scale aggression, most of the industry’s indicators fell by two to three times. The main losses of the iron and steel industry as a result of the war include the following:

Other industry indicators also declined. According to the FMU, the number of employees in the sector fell by almost half, from 122,000 at the beginning of 2022 to 62,000 at the end of 2025.

At the end of last year, for the first time since 2023, steel production began to decline again, falling by 2.2% year-on-year – to 7.4 million tons. The downward trend in production continued in 2026: in January-February, steel production decreased by 13% y/y. This was due to power shortages and high electricity prices, as well as the negative impact of CBAM.

Ukraine’s iron and steel industry is a key player in the post-war recovery of the economy, infrastructure, and the entire country. Steel is the basic material for post-war recovery. The implementation of at least part of the recovery programs creates huge domestic demand for construction steel products.

According to GMK Center estimates, additional demand for steel during the recovery period will range from 1 to 3 million tons per year, depending on the economic development scenario. The most sought-after items are rebar and wire rod (residential construction), flat-rolled products (industrial construction and infrastructure), and shaped rolled products (bridges).

GMK Center estimates indicate that Ukraine’s existing steel capacity is sufficient to meet the demand for the main types of steel products for post-war recovery.

Currently, companies in the industry are forced to reduce their production capacities. For example, ArcelorMittal Kryvyi Rih has decommissioned its blooming shop and suspended the production activities of its subsidiary, Livarno-Mechanichny Zavod LLC. The reasons for this are the high costs of CBAM and expensive electricity, which make Ukrainian products uncompetitive in export markets. For much of the fall-winter season of 2025/2026, Interpipe’s steelmaking facilities were idle due to the consequences of shelling of Ukraine’s energy infrastructure.

Domestic production in Ukraine will not only ensure uninterrupted supply of the necessary range of products, but also reduce the cost of recovery by cutting imports, support tens of thousands of jobs, and contribute to replenishing budgets at all levels with tax revenues.

Supporting the iron and steel industry now, or at least not creating new obstacles in the form of tariff increases and other administrative measures, will cost the state significantly less than rebuilding the industry from scratch after the war or financing imports of everything necessary.

Source:GMK Center