Posted on 28 Apr 2023

Message from the Secretary General: ASEAN’s Direction for Climate Change

Climate Change Impacts

In the Southeast Asia Climate Outlook 2022 survey report by the Yusof Ishak Institute of South East Asia Studies (ISEAS), respondents were very concerned floods (22.4%), heatwaves (18.1%) and rainfall induced landslides (12.0%). Given the diverse nature of ASEAN’s geography, climate impacts are also diverse from concerns about drought (Laos 22.8%) to worries about tropical storms (24.8%).

Most respondents believe that food supply disruptions are mainly due to:

- Extreme weather events (31.2%)

- Global supply chain disruptions (25.3%)

- Reduced food exports from producer countries (19.1%)

Those living in rural areas are most concerned about the threat of extreme weather events (46.8%). Those in the midsize cities and rural areas are very concerned about degraded farmland (22.1%).

As such, most ASEAN governments have set net zero targets:

- 2065 : Thailand

- 2060 : Indonesia

- 2050 : Brunei, Cambodia, Laos, Malaysia, Singapore, Vietnam

- 2040 : Myanmar (partial)

- None : Philippines

ASEAN Climate Change Pathway

The ASEAN State of Climate Change Report (“ASEAN [2021]”) is the most comprehensive document that lays out climate change issues, existing policies and pathways towards climate change goals in ASEAN.

What ASEAN needs to do fall in 2 broad categories:

- Climate change adaptation, which is the process of adjusting to the impacts of climate change

- Climate change mitigation, which is reduce or prevent the emission of greenhouse gases to lessen the magnitude and impacts of climate change. This part is most relevant that is applicable to the steel industry.

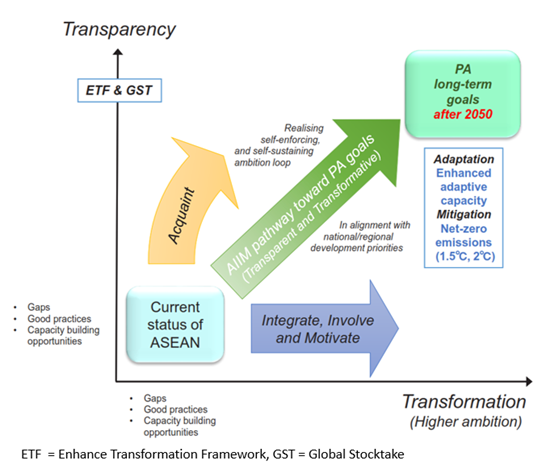

The pathway for ASEAN to achieve its Paris Agreement commitments consist of 4 groups of actions (see figure 1 below):

- Acquaint: knowledge enhancement through data collection, analysis and monitoring

- Integrate: coordination of efforts across governments, ministries, departments, sectors

- Involve: involvement of all stakeholders

- Motivate: incentives (finance, technology, others) for the stakeholders to act

Figure 1. ASEAN climate vision toward 2050, showing the AIIM pathway to achieve the Paris Agreement goals of adaptation and mitigation. ASEAN [2021].

Key Sectors for Mitigation

Since climate change mitigation efforts are more relevant to the steel industry, this article will focus on mitigation efforts and not on adaptation efforts.

ASEAN governments have identified the key sectors for mitigation intervention (in order of priority):

- Energy (coal / gas plants, renewable energy, others). Efforts on renewable energy are underway, although it is at early stages in ASEAN.

- Transport (public transport, biofuels

- Industry

- Agriculture, Forestry and Land Use

High Priority Technologies List

ASEAN has identified high priority technologies across many sectors and the following is the list of related sectors to the steel industry (towards 2030 and 2050 & beyond:

1. Decentralised Energy

- Variable Renewable Energy or VRE (solar, onshore and offshore wind), advanced energy storage system, demand-side management, smart and mini grid

- Scale up of the high priority technologies, plus grid enhancement to accommodate increased Variable Renewable Energy (VRE)

2. Industry Energy (Fuels)

- Higher efficiency of conversion process of fossil fuels

- Biofuels, Bio Energy with Carbon Capture and Storage (BECCS)

3. Industry Energy (Gas System)

- Low-carbon hydrogen (e.g. hydrogen by electrolysis with RE), synthetic methane from low-carbon hydrogen, cleaned biogas (BECCS)

4. Industry Process (Iron and Steel)

- Energy efficiency improvement

- Carbon Capture, Utilisation and Storage (CCUS), low-carbon hydrogen, biomass, circular economy

5. Road Freight

- Higher efficiency internal combustion engine (ICE), biofuels, battery charge

- Electrification (EV), low-carbon hydrogen (FCV), biofuels

6. Shipping

- Higher fuel efficiency, LNG bunker

- Synfuels from green hydrogen (CCU), biofuels, electrification, ammonia

ASEAN Mitigation Action Plans for Transformation

To transform the key sectors ASEAN has also set a series of broad direction to transition towards a low carbon future. Relevant to the steel industry are these 3 main areas (within the Motivate group of actions):

A. Finance

- Enhance access to international mitigation finance

- Establish an ASEAN central fund specific for ASEAN's mitigation needs

- Facilitate innovative finance to shift paradigm of future business (private sectors)

B. Technology

- Enhance access to international mitigation technology (low- or zero carbon)

- Promote R&D for innovative clean technology development

- Enhance technology diffusion of mitigation (low- or zero-carbon) through incentives and innovative policy framework

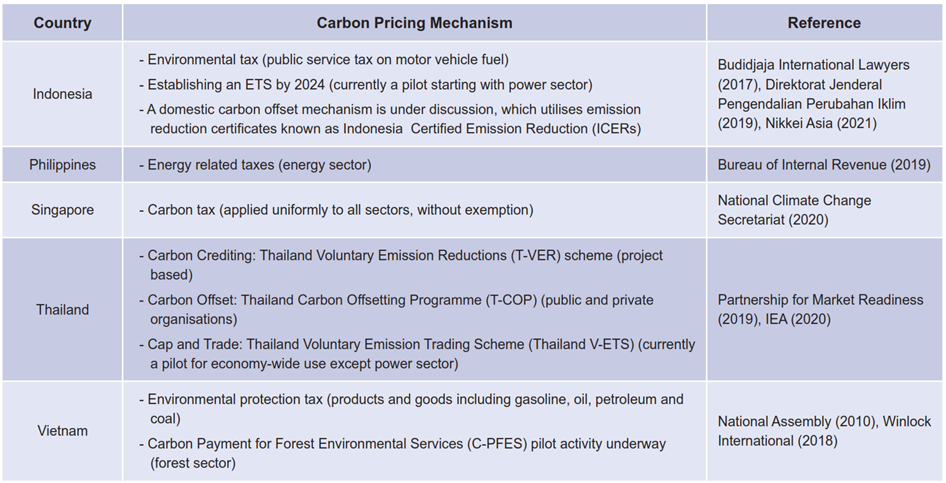

C. Carbon Pricing (See figure 2 on ASEAN carbon pricing systems at the end of this article)

- Share lessons learned on carbon pricing systems through documentation of best practices, gaps, challenges etc.

- Introduce and strengthen carbon pricing at the regional, subregional and national level

What’s Next for the ASEAN Steel Industry?

ASEAN may appear to be “quiet” in terms of climate change actions, but in reality, the governments are planning for a low carbon future. What you do not see now, does not mean nothing is happening. It means the undercurrents are forming and it is time to build/upgrade your ship to ride the upcoming waves.

So, what should the ASEAN steel industry do? Here are some of the areas for consideration:

I. For the ASEAN Steel Industry in General

- Prepare a long-term plan to transition towards a low carbon emissions future, in line with country net zero targets

- Measure scopes 1, 2 and 3 emissions and make plans / take steps to minimise emissions

- For those with old and inefficient equipment, it may be worthwhile to look at upgrading projects (now or future) to achieve energy savings, process improvements, cost reductions, carbon reduction and other necessary targets.

- Explore upgrading efforts and generating carbon credits simultaneously. This can be done through joint government collaboration and other potential financing schemes where available

- Use alternative energy, where possible, such as renewable energy (solar power) as well as use of higher quality materials that reduce emissions

- Continue to keep up to date on technology development and financing schemes for low carbon technology investments

- Start exploring the carbon markets and seek out high quality carbon credits. The need to buy carbon credits may come faster than the technology to reduce emissions.

II. For Investors (Steel Projects) in ASEAN

- ASEAN steel industry is in an overcapacity situation today. With the numerous new blast furnace projects being proposed or under construction, the region will be in severe overcapacity before 2030.

- For those planning to invest in ASEAN, pay particular attention to segment demand supply situations. In general, the ASEAN long products sectors are in overcapacity. Investors should target segments that are not in overcapacity.

- It is essential to bring the latest technology that is not carbon intensive, or to include Carbon Capture, Utilisation and Storage (CCUS) equipment to minimise emissions

III. For ASEAN Steel Industry & Governments

Discuss with your governments on funding and incentives to upgrade your equipment to reduce emissions. These will be made available in due time

There is a need to develop demand for low carbon materials. Imposing carbon taxes is easy, but this will affect demand. Governments should create demand for green products through their public procurement policies and incentivise the use of green materials one way or another.

- Work with governments on preventing carbon leakage, to implement carbon border taxes on imported high carbon materials

So there you have them, a quick look at climate change impacts and policy directions in ASEAN and some of the key areas the ASEAN steel industry should be looking at towards 2030, 2050 and beyond.

Stay Healthy. Stay Safe.

See You at SEAISI Events.

ISEAS [2022] Southeast Asia Climate Outlook 2022 Survey Report. Available at: https://www.iseas.edu.sg/articles-commentaries/southeast-asia-climate-outlook/southeast-asia-climate-outlook-2022-survey-report/ (accessed: Mar 2023)

ASEAN [2021] ASEAN State of Climate Change Report. Available at: https://asean.org/book/asean-state-of-climate-change-report/ (accessed: Jan 2023)

Figure 2: Carbon Pricing in ASEAN (ASEAN [2021])

Source:SEAISI