Posted on 28 Sep 2022

Why Are Commodity Prices Rising?

Global events and certain regional events in history are impacting commodity markets and prices.

The COVID19 pandemic led to a sharp fall in demand as lockdowns reduced mobility and consumption, disrupted supply chains and curtailed manufacturing activities. Supply of materials, including commodities were cut and workers laid off. Businesses were and still are under extreme pressure; some went bust.

Investments were postponed, also adding to lower potential supply.

As restrictions were lifted, demand rebounded sharply. However, supply could not catch up due to capacity and supply constraints. ASEAN countries depending on foreign labour, face manpower crunch, stalling construction manufacturing and construction activities.

Continuing disruption at the “world’s factories” in China also affected material supply as China enforces its zero COVID policies, locking down cities, businesses and ports.

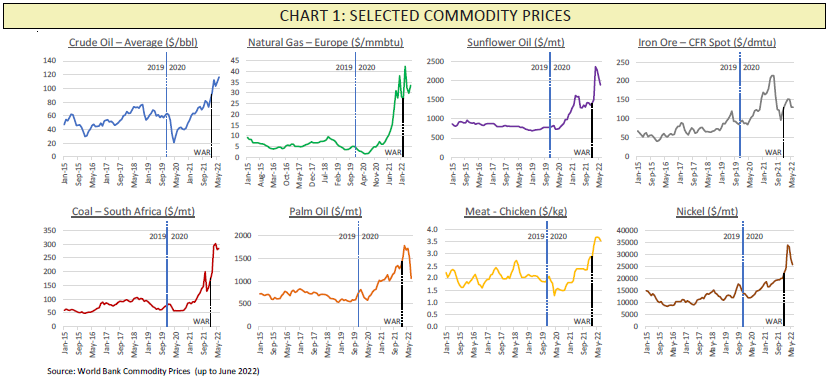

However, iron ore prices did not quite follow the other commodity prices. Instead, iron ore price movements are also affected by demand and supply fluctuations for steel in China; China is the largest producer of steel and the largest buyer of iron ore.

That was before the war. Commodity prices were already rising rapidly due to pent up demand, even before the Ukraine war, as shown in the Chart 1 at the end of this article.

The Russian invasion of Ukraine sparked off further commodity price increases, worsening supply chains disruptions, increasing food insecurity, leading to higher inflation.

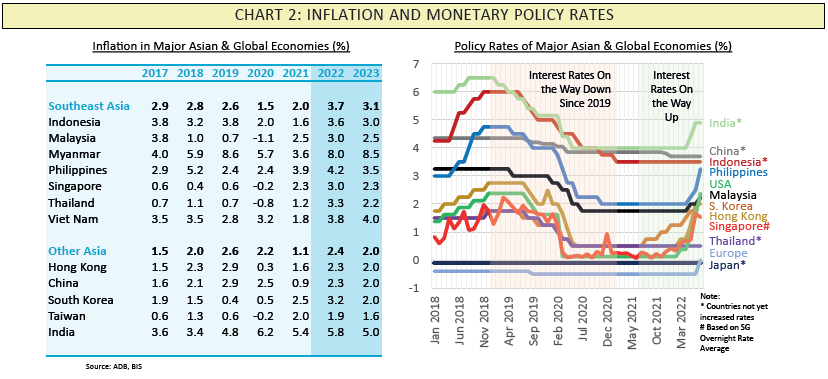

The ADB has forecasted that the ASEAN and major Asian countries to experience elevated levels of inflation for 2022, with 2023 inflation easing in most countries except Myanmar and Vietnam (Chart 2). With no abatement in sight, inflation is expected to be higher than forecasted in 2022.

The “Fed-Induced Inflation”

Over the last few months, the US Federal Reserve Board (Fed) has been hiking US interest rates to control the rampant rise of inflation across the United States.

On 27 July 2022, the Feds hiked interest rates by 0.75%, a huge jump after a previous large 0.5% hike on 4 May 2022. The May hike was already considered to be the biggest hike in 2 decades, deemed necessary to tame the highest inflation rate in 40 years. Note that inflation was 9.1% in the 12 months ending June 2022. The Feds have indicated there could be another hike in September 2022.

The rising interest rates in the US has triggered an outflow funds from regions across the world, including ASEAN. This has further weakened many major currencies in Asia. Weaker currencies mean imports will become more expensive.

On 26 July 2022, before the Fed’s 0.75% rate hike, the Indonesian rupiah lost 5.5% versus the US dollar compared to 1 Jan 2022. Malaysia ringgit devalued 7%. It was 8.8% for Philippines and 10.5% for Thailand. For Singapore, it was back to 3.3%, erasing the gains from the tightening of monetary policy on 13 July 2022. Both Indonesia and Thailand have yet to increase interest rates.

The recent 0.75% Fed interest rate hike is expected to further weaken ASEAN currencies should these countries not tighten their monetary policies accordingly.

Monetary Policy Tightening in ASEAN

Increasing interest rates has the effect of cooling overheating prices as it discourages spending and encourages savings. It also increases the cost of debts to individuals and businesses. While the hikes are to control inflation, ultimately economic growth is affected.

So far, Malaysia has increased interest rates by 25 basis points (0.25%) in May and July 2022 each time. The Philippines raised its key interest rates by an aggressive 75 basis points (0.75%) in July 2022, following an earlier 25 basis point adjustment a month earlier.

Singapore tightened its monetary policy through exchange rate settings instead of interest rates in October 2021, January and April 2022. A further off cycle tightening of monetary policy in July closed the gap with the US dollar but the recent hike erased all the gains.

Many other major Asian economies have been hiking interest rates too, such as South Korea and Hong Kong. Europe and UK are also increasing interest rates.

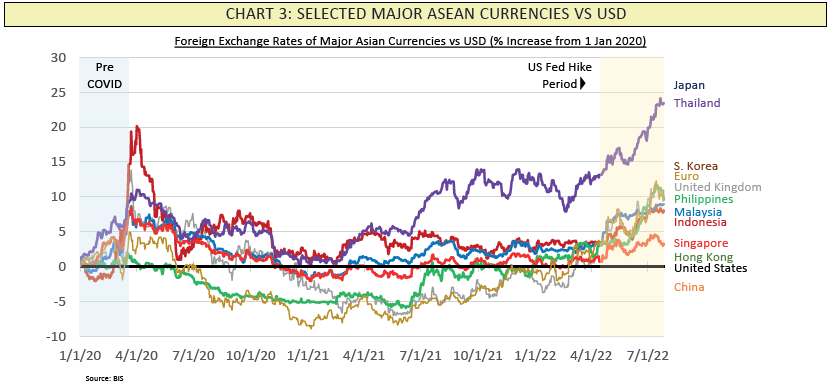

With inflation showing no signs of retreating this year, it would not be surprising to see further increases in interest rates across the world. Chart 3 shows many major Asian economies, including ASEAN countries experiencing weakening currencies against the US dollar.

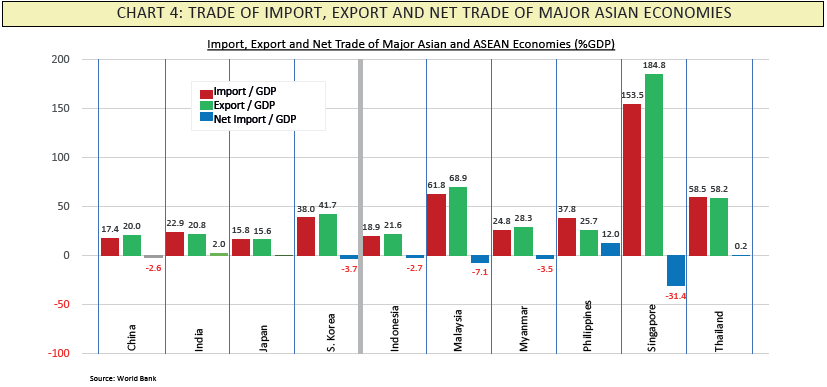

Logically, countries that have strong domestic industries would experience lower imported inflation rates, while those that have large imports would experience higher imported inflation rates. Countries such as Singapore, that rely on trade would need to follow its trading partners’ rate hikes to some extent. Chart 4 shows countries with high percentage of imports per GDP.

Whether or not the other ASEAN countries will follow the hikes by the Fed is complex process. Certain countries are fighting inflation through price controls and subsidies, and not just interest rates alone. In many ASEAN countries, prices of cooking oil, energy costs and certain food commodities are controlled or these are subsidised. Regardless, fund flows tend to follow interest rate changes more than price controls, thus affect a country’s foreign exchange to some extent.

Implications

In July, World Bank and IMF all released their forecast for the world, major Asia and South East Asia economies. As expected, with the rising inflation, increasing rates, ongoing war and continuing impact from COVID variants, it is not surprising that both agencies have revised global growth downwards from their previous projections.

World Bank reduced the 2022 global growth to 2.9% from 4.1%. Similarly the IMF reduced global growth to 3.2% from 3.6%. If this trend continues, a few countries will face the risk of recession. All these are not good as global economies are trying to recover from COVID19.

Next month, ASEAN governments will release their Q2 2022 macroeconomics data. We shall see then, how the countries are performing amid the current challenges.

Get Vaccinated. Get Your Booster.

Keep Your Distance. Wear Your Mask.

Stay Healthy. Stay Safe.

(Yes, I know. Global borders are re-opening, with fewer restrictions. But the pandemic is not over and we need to stay safe, for a little while longer)

Source:SEAISI